1. Introduction

In 2015 the Cyprus property market turned into a conflict arena for strong counterforces. Negative influence has been exerted by both the reduction in the purchasing power of Cypriots and Russians, as well as the massive problems Cypriot developers face with their non-performing loans. On the other hand, the significant improvement of the macroeconomic indicators for the Cyprus economy, the growth in tourism, the boost for the purchasing power of the British and the pound sterling, have all contributed to the growing interest for holiday homes in Cyprus. As a result of all the aforementioned, the steep drop of the Residential Property Price Index is being mitigated while sales have increased, thus creating favorable prospects for the future.

2. Signs of Recovery for the Cyprus Economy

2.1. Macroeconomic indicators

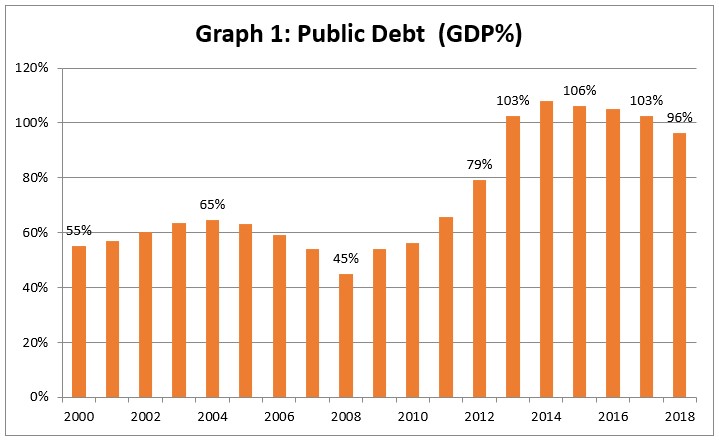

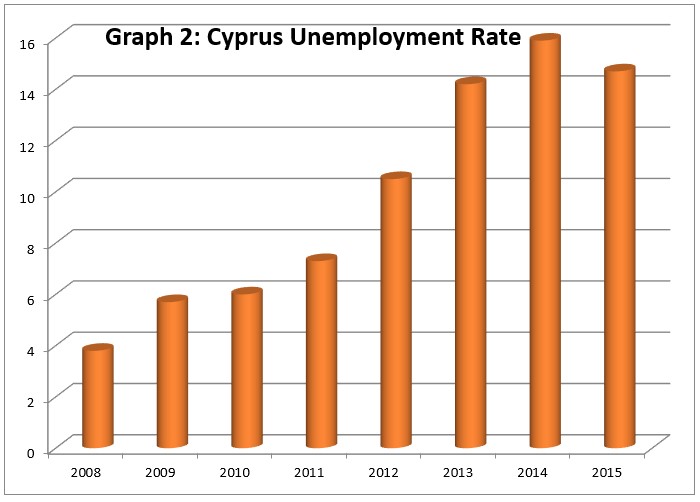

The collapse of the banking system in March 2013 forced the Cyprus government to request financial aid from the European Stability Mechanism (EMS). For Cyprus, joining the EMS meant the signing of a Memorandum of Understanding with the troika, which required the implementation of immediate reform and countercyclical fiscal policies. In the years 2012-2014 Cyprus saw an immense increase in its public debt from 79% to 108%, while unemployment rates skyrocketed from 10.5% to 15.9% (graph 1 and 2).

Despite the recession measures and heavy taxes, in 2015 there was an improvement in all the main economic indicators. In particular, GDP is expected to increase between 1% - 1.5%, while for 2016 the Ministry of Finance is expecting growth rates close to 1.8%. Public debt has decreased for the first time since 2008 and it is expected to come down to under 100% as a GDP percentage after 2017. The government’s determination to implement immediate reform at any political cost has contributed to the upgrade of both the country’s credit rating and its banking institutions by international credit rating agencies. This, in turn, has helped reduce the interest rate on the public debt from 4.2% in 2012 to 3.1% in 2015.

2.2. Financial System

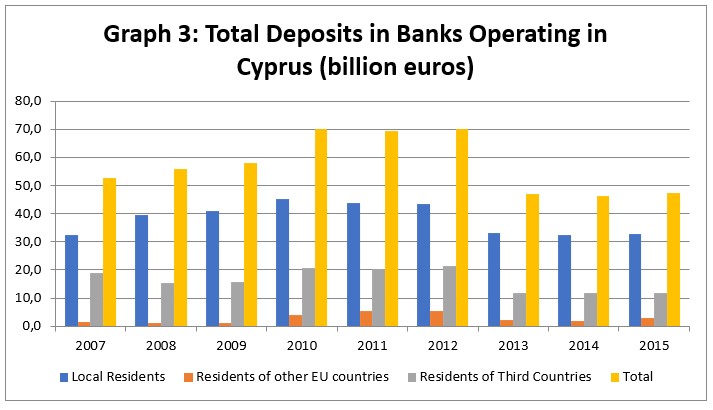

The banking system continues to be the sick man of the Cyprus economy. What is making the banking institutions’ attempt of asset reorganization challenging is the massive number of non-performing loans. The unexpected bail-in of bank deposits (haircut) has shaken citizen trust, leading to a disconcerting deposit outflow during the years 2013-2014 (the level of deposits was reduced by 35%). This negative disposition seems to be overturned in 2015, with the total level of deposits increasing by 3% (Graph 3).

The course of the banking system affects the property market in three ways:

- Borrowing cost (housing loans)

- Divestiture law and Insolvency

- An alternative form of investment

2.2.1. Borrowing cost

Right after the haircut, the largest Cypriot banks increased borrowing from the ELA (Emergency Liquidity Assistance) and went ahead with a successful recapitalization.

In the autumn of 2014, the banking institutions and the cooperative bank successfully underwent Stress Tests from the European Banking Authority and the European Central Bank. Moreover, the Bank of Cyprus, which still possesses the lion’s share in the banking market, successfully reduced its ELA funding from €11.4 billion in 2012 to €5.5 billion in 2015.

In cooperation with commercial banks, the European Investment Bank has also contributed to the general attempt to finance the country’s economy by providing small and medium-sized companies with low-interest loans.

Another important factor that significantly affects the granting of mortgage loans is the reduced strictness concerning funding criteria. From 2010 until the first semester of 2013 there was a tightening of lending criteria when it came to the granting of mortgage loans. In 2015, these criteria have been limited, allowing banks to offer more flexible credit provision proposals to borrowers.

At the Eurozone level, important decisions that are favorable for the reduction of lending costs have been taken. In particular, the European Central Bank (ECB) has kept the base interest rate at 0.5% because of low growth rates within the Eurozone (0.8% for 2014 and 1.5% in 2015). At the beginning of 2015, the Governing Council of the ECB decided to initiate the Public Sector Purchase Program in the secondary markets. This decision contributes to the strengthening of the economy while at the same time it helps stabilize the banking system.

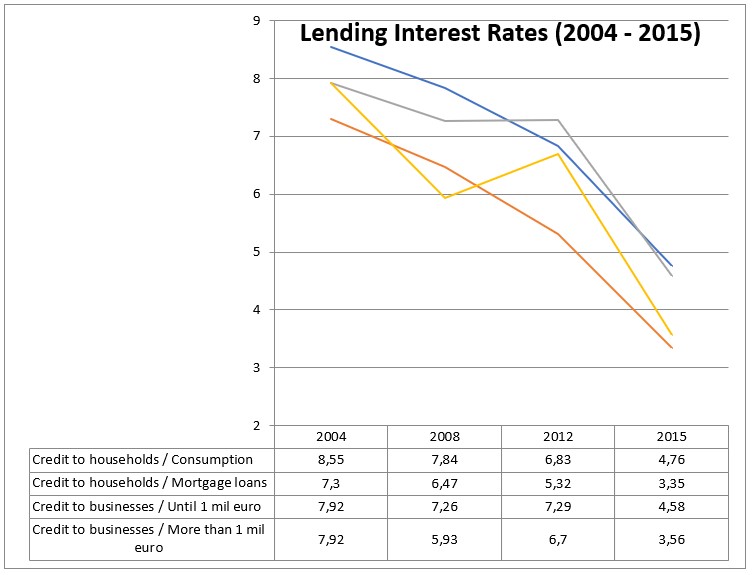

All these factors on a national and European level have contributed to the significant reduction of loan interest rates, as can be seen in Graph 4. Specifically, based on statistical data from the Central Bank of Cyprus, housing loan interest for 2015 was 3.5%, which is a percentage point lower than that of 2014.

2.2.2. Divestiture Law and Insolvency

Despite the significant reduction of interest rates, the high percentage of non-performing loans is one of the main reasons why banks are particularly cautious with credit provision processes. Within 2016 banks should use the restructuring tool more intensively in order to provide motives for borrowers to meet their obligations.

Divestiture law is a particularly important tool in the consolidation effort of banking assets. Nevertheless, the expected wave of massive divestitures has frozen investors’ interest, since they anticipate an equally massive price collapse. If they do not want to crash the market, banks should create property investment packages that will subsequently be securitized and exclusively promoted to investment funds abroad.

2.2.3. An Alternative Form of Investment

The haircut on deposits has been a determining factor in shaping Cypriots’ investment behavior. The massive problems of the banking system have made Cypriots particularly suspicious about the banks’ ability to protect their deposits. Because of its material and tangible nature, for many investors, the property market constitutes a safe refuge for their savings. This is one of the main reasons why in the first semester of 2014, domestic demand for property increased by 26.1% compared to the first semester of 2013, despite the economy’s collapse. The significant increase in sales in the domestic market continued in the first semester of 2015 with a percentage of 6.3.

An important role in the upgrade of property as an investment solution was also played by the Central Bank of Cyprus’ decision in February 2015 to decrease the highest deposit interest rate by 100 basis points, from Euribor +300 to Euribor +200. The reduction of the highest deposit interest rate, ultimately aiming to increase liquidity, has led to a substantial decrease in the deposit interest rates of commercial banks and has consequently made deposit deals less attractive.

2.2.4. Reduction of Bank Credit

Despite the remarkable decrease in loan interest rates, the significant decline of household and businesses’ purchasing power combined with the increased uncertainty about the future contributed to the reduction of credit provisions for 2015. Specifically, the provision of credit in the private sector went down by 2.2% in July 2015 compared to the same period of the previous year. The reduction is noteworthy but lower than the 8% decrease that happened in 2014. Mortgage loans that were a determining factor for the property market growth in the golden era of 2000-2007 also decreased by 2.4%.

3. International Developments

3.1. Tourism and Permanent Residence

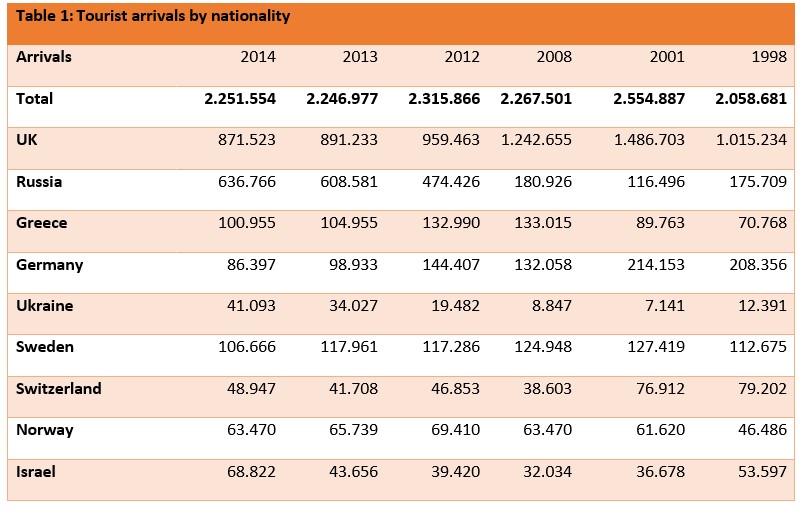

Cyprus is one of the top Mediterranean tourist destinations since it annually welcomes about 2.3 million tourists (Table 1).

Charmed by the natural beauty of the island, a big number of tourists decide to purchase a holiday home. Up until 2004, this market was monopolized by British pensioners. Paphos was the district that housed the biggest English-speaking community in Cyprus, given that in the last population census of 2011, 12% of the district population were UK nationals. The financial crisis of 2008 and the depreciation of the pound sterling against the euro led to a decline in the purchasing power of the British and the subsequent decrease in property sales in Cyprus. In order to balance out the negative consequences while taking advantage of Cyprus joining the EU in 2004, the government-initiated programs through which it grants permanent residence and citizenship to third-country nationals through investment. These programs are still highly successful, with the greatest interest shown by Russian, Ukrainian, Chinese and Arab investors.

3.2. The UK Economy

The UK is one of the first western countries to escape the 2008 financial crisis. The country’s GDP had growth rates of 2.9% and 2.2% in 2015 and 2014 respectively. Despite its constant fluctuation in the last 5 years, the pound sterling has improved its exchange rate against the euro by 11%, while in the summer of 2015 the revaluation had reached up to 30%. There were substantial developments in the property market as well, with the average price index showing an increase of 20% in 2014 and 13% in 2015.

All of the above factors point to a substantial increase in the purchasing power of British nationals, which is why we should expect the interest in the Cypriot property market to remain unabated.

3.3. The Russian Economy

Russia has been the most important source of Foreign Direct Investments (FDI) in Cyprus since 2008, which was when Cyprus joined the Eurozone. Thousands of Russian businesses have a tax base in Cyprus while in the last ten years a big portion of these companies has also established a physical presence on the island. Wealthy Russian nationals have bought a second home in Cyprus and through a fast-track procedure have been granted permanent residence or citizenship.

These outstandingly good relations, not shaken even during the deposit haircut, are facing two challenges. The annexation of Crimea from the Russian Federation on 18th March 2014 led to two-way financial sanctions between Russia and the EU. The autonomist tendencies of the Russian-speaking regions in Eastern Ukraine are very likely to cause a worsening in Russian-European relations and to the imposition of new financial sanctions. These sanctions mainly affect the export of Cypriot agricultural products and are not expected to have any major impact on the banking and tourism sectors.

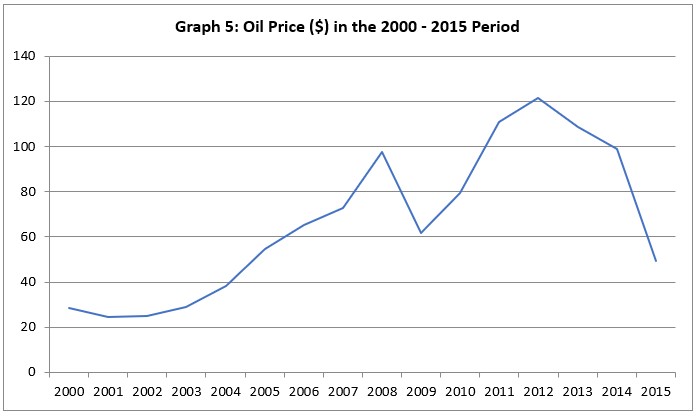

The second challenge concerns the continuous devaluation of the rouble against the euro. Between July 2014 and January 2016 the euro was revaluated against the rouble by almost 100%. The rouble’s decline is directly connected to the collapse of oil prices (Graph 5), which is expected to continue in the next two years because of OPEC’s high production policy and the slowing down of the Chinese economy.

The significant decrease in Russians’ purchasing power will undoubtedly be reflected in the Cypriot property market. In 2015 the interest of Russians in property has already significantly subsided, with the English and Chinese market leading the sales increase.

There are, however, encouraging signs from the tourism sector. The shooting down of Russian Sukhoi Su-24M aircraft from a Turkish Air Force jet on 24th November 2015 had, as a result, the deterioration of Russia-Turkey relations and the signing of a presidential decree which banned chartered flights to Turkey, prevented tour firms from selling holiday packages there and halted the existing visa-free regime between the two countries. Russians who visited Turkey in 2014 and 2015 amounted to 4.5 and 3.6 million respectively. This huge tourist flow is expected to go down by up to 60%, not just because of the presidential decree but because of the increased danger of a terrorist attack on Turkish ground.

The heightened danger of a terrorist act is also the reason for a substantial decrease in Russian flights to Egypt. On 31st October 2015, the ISIS terrorist group placed an explosive device on Russian flight 9268, leading to the airplane’s crash in Sinai and the death of 224 people. Russia immediately issued a decree by which it canceled all flights to Egypt.

All of these events resulted in Russian travel agencies starting to direct tourists away from Turkey and Egypt and towards European destinations like Cyprus, Greece, Spain, and Italy.

4. Property Price Changes

4.1. Residential Property Price Index Changes

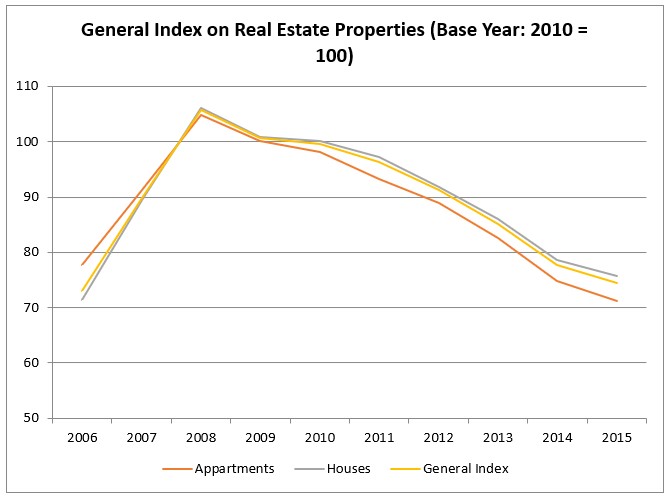

Despite the significant increase of demand from the domestic market and the steadily high interest for property in tourist areas by foreign country nationals, property prices continue to drop for the seventh year in a row, reaching the levels of 2006 (Graph 6). During 2006-2008 the property market in Cyprus turned into a financial bubble environment, whose creation was enabled by the uncontrolled granting of mortgage loans by banking institutions. In financial terms, the current period of the property market could be characterized as a “period of correction” or a “period of rationalization” of supply and demand.

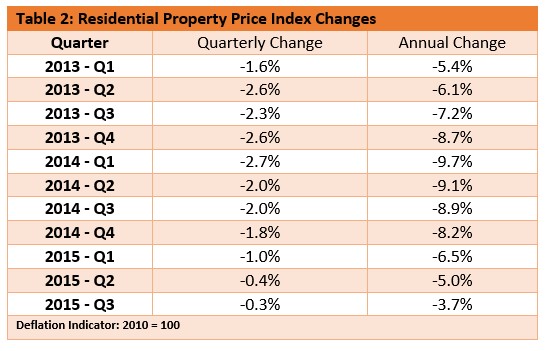

As can be seen in Table 2, the steep drop in prices during 2013-2014 has started being contained in 2015. Specifically for the third quarter of 2015, the price drop was restricted to 3.7%. The massive annual drop in prices in 2014 has been succeeded by a smaller decline of 4.2%.

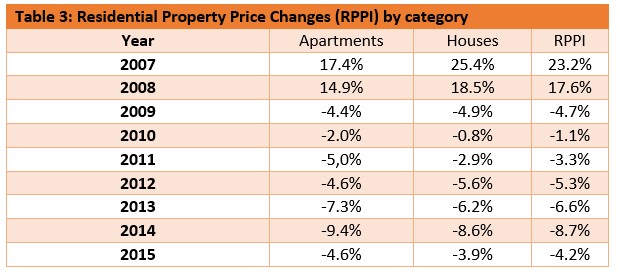

Table 3 analytically shows how prices have changed in the house and apartment market. It can be observed that in the last three years, apartment prices have undergone a comparatively bigger reduction, making this market particularly attractive for prospective buyers.

4.2. Average Property Price Changes by District

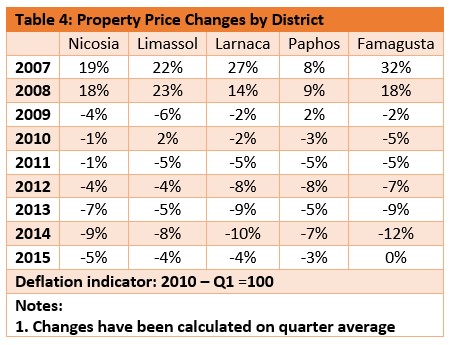

If we examine property prices on a district level (Table 4) we can see that macroeconomic conditions symmetrically affect property prices in all districts.

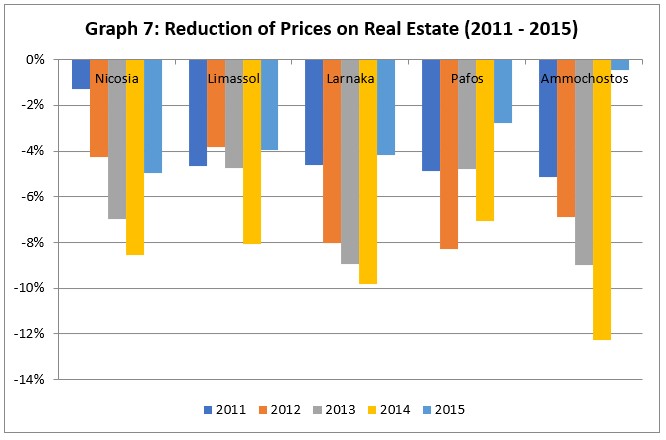

In Graph 7 below, we focus on a comparative analysis of property prices in different districts during the period of economic recession 2011-2015.

As can be seen in the graph, 2014 was the year with the highest annual decrease for all districts. The only exception was Paphos, which experienced mass sales from English pensioners in 2012 due to the difficult financial situation in the UK. Paphos, as seen on the graph, is nevertheless the district whose property market also shows the strongest signs of stabilization.

Because of the high demand for holiday homes by Russian nationals, the Limassol district had a comparative smaller reduction. The demand for luxury property in tourist areas because of the citizenship through investment program kept the steep price drop observed in other districts under control. An important factor for market stabilization in Limassol was the interest in office and other commercial property rentals. The high demand for offices and luxury homes contributed to obtaining funding for big investment plans, like the Oval of the Cybarco Company and the ONE skyscraper by the Pafilia Company.

2011-2014 was a particularly challenging period for Larnaca and the Free Famagusta district, with the latter going through the most significant annual decrease of all the districts in 2014 when it saw its property prices collapsing by 12%. Famagusta, which is highly dependent on seasonal tourism of a low-income scale from Russia, was particularly affected by the notable devaluation of the rouble. The significant property price reductions contributed to the creation of exceptionally good investment opportunities, resulting in an increase of supply while the prices remain unchanged for 2015. The massive tourist influx expected from Russia for 2016 will contribute to the increase in demand for holiday home rentals and ceteris paribus will contribute to a substantial increase in apartment prices.

5. Number of Sale Contracts

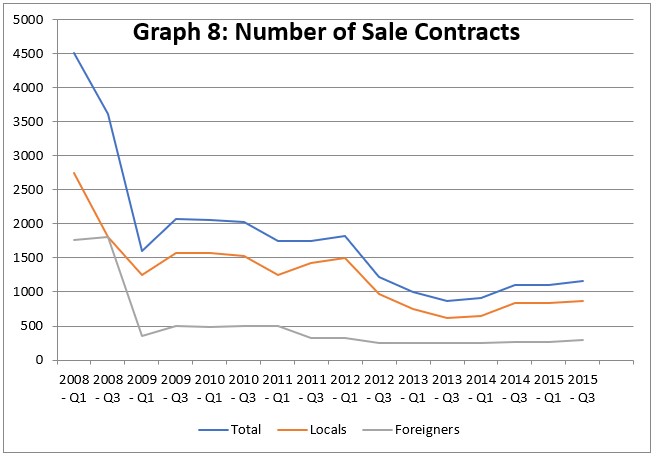

As can be seen in Graph 8, the significant drop by 8.7% in the Residential Property Price Index in 2014 contributed to a surge of sales in the same year. This was mostly due to the increased property demand by Cypriots.

In 2015 the favorable climate for sales continued, recording an increase of 6% for the third quarter. Specifically, purchases by Cypriots increased by 2.7% while purchases by foreigners skyrocketed, increasing by almost 16%.

6. Rentals

6.1. Average rent

The rental sector is one of the most important parts of the property market since the financial crisis has contributed to a revitalized interest in it. The massive tourist flow expected to be directed to Cyprus in 2016 turns the property that will be used for tourist rental into significant investment opportunities.

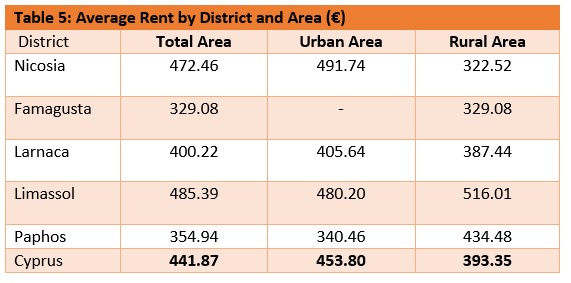

Table 5 presents the average rent by the district. As can be seen on the table, the highest rent is recorded in the Limassol district and the lowest in the Paphos district. In rural areas, the Limassol district remains the most expensive, with Paphos following it due to the high demand for residences from long-term renting tourists.

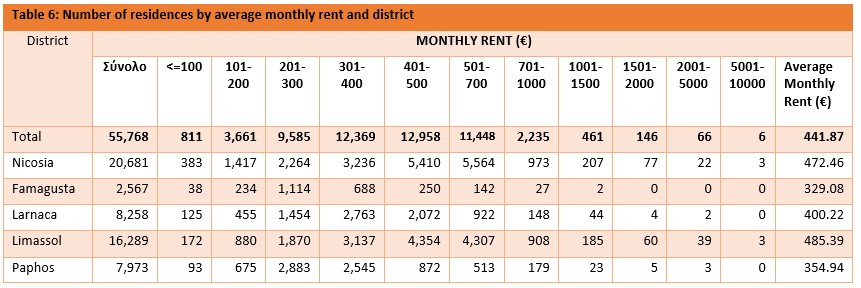

Table 6 presents the number of residences by district and by average monthly rent. It appears that the vast majority of residences are rented for between 200 and 400 euros per month.

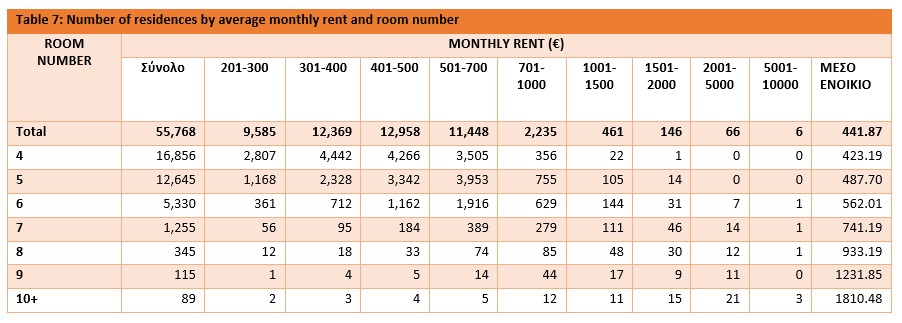

The table below shows the average rental cost depending on the average rent and room number.

6.2. Rental market prospects

The rental market in Cyprus is expected to generate immense interest in 2016 for the following reasons:

- The unstable situation in Arabic countries because of the Arab Spring and the fear of a terrorist attack is expected to contribute to the increase of tourist flow towards Cyprus and other European countries on the Mediterranean Sea.

- The deterioration of Russian-Turkish relations will be a factor that should significantly push massive tourist flows to Cyprus. Big tourist agencies like Biblio Globus have already signed new agreements to transfer tourists from Turkey to Cyprus.

- The strengthening of the pound sterling and the improvement of macroeconomic conditions in Britain are expected to bring about the return of English pensioners and younger people to the tourist areas of Paphos and free Famagusta.

- The high unemployment percentage and the reduction of Cypriots’ purchasing power mean that there is a transition of interest from house purchases to apartment rentals.

7. Cost of living and other relevant indicators

Low property prices, lower demand and the inability of many construction companies to pay off their loans continue to significantly affect the construction sector. Local sales of cement recorded an annual increase of 6.8% during the third quarter of 2015, compared with an annual decrease of 13.7% in the same quarter of the previous year. The price index of construction materials reduced on an annual basis by 3.2% in the third quarter of 2015. The decrease is mainly due to the major drop in oil prices since oil is a basic production factor in the construction process (Graph 5).

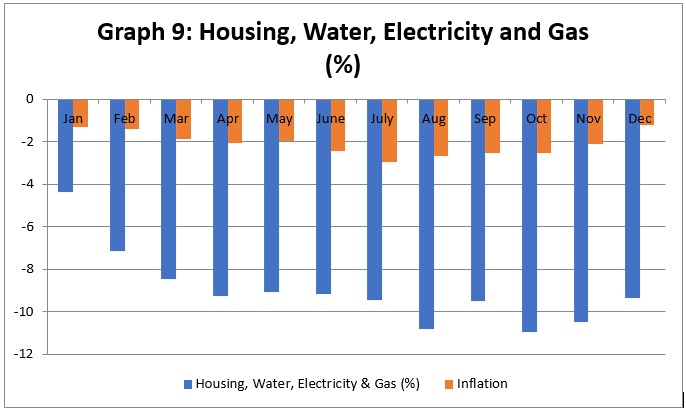

A significant decrease was also observed in the cost of living in Cyprus during 2015. As can be seen in the diagram below, the cost of living, water, electricity, and gas (compared to the cost of the same months in 2014) has become lower than the Consumer Price Index.

8. Improved framework for the issuance of title deeds

Until today, the yeasty functioning of the property market was impeded by the underdeveloped title deeds issuance system. Unfortunately, buyers were often trapped in time-consuming bureaucratic procedures that stopped them from issuing their title deeds, either because the property was mortgaged by the seller or due to the fact that the seller owed tax to the state. To face this problem, the government has forwarded a relevant bill for structural changes that will make the process of issuing building permits more efficient. This is expected to restore confidence in the Cypriot property market, making the property more attractive.