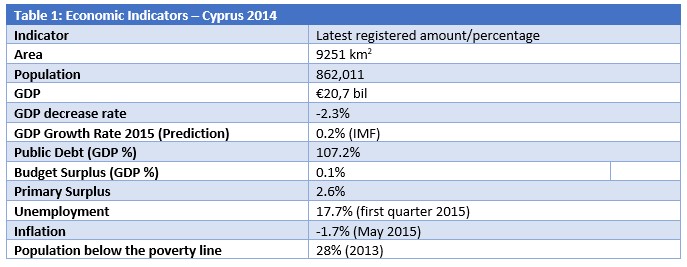

1.Table of Economic Indicators

2. Introduction

In 2014, the Cypriot economy seems to have overcome the bankruptcy peril that was created after the deposit haircut of March 2013. The stabilization of the banking system combined with the improvement of other socioeconomic factors indicates that Cyprus is undergoing massive recovery efforts. However, the way towards the stabilization of economic indicators will be a painful one due to the intrinsic flaws of the system.

3. The factors on which the Cypriot economy’s recovery is based on

3.1. Stabilization of the banking system

Despite the enormous liquidity problems, they faced following the unprecedented experiment of the bail-in, Cypriot banks have successfully executed their recapitalization program. The banks have significantly restricted their exposure to the Greek debt crisis while partly regaining depositors’ trust.

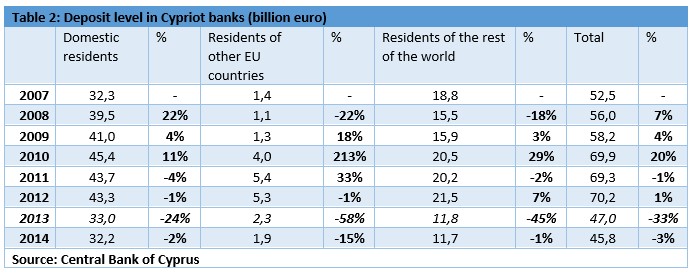

Table 2 shows the total value of deposits in Cypriot banks for 2007-2014, as well as their annual change. Deposits had reached their highest level in 2012, with a total of 70.2 billion euro.

As is evident, the deposit outflow that started in 2013 has been significantly limited. In particular, during 2014 the deposits of Cyprus tax residents have gone down to 2% compared to 24% in 2013. In the case of deposits from residents of other countries (the lion’s share of which is from Russian depositors), deposits have decreased by 1%. In total, the decrease in deposits during 2014 has reached 3%.

If the stabilization of the banking system is to continue, this is largely dependent on the materialization of the divestiture program, which was one of the main terms set by Troika in order to give Cyprus a funding package. Despite the numerous bureaucratic and legal barriers, the divestiture program has already been in effect since September 2014 and is expected to mitigate bank liabilities.

Another determining variable in the consolidation path is the way non-performing loans are managed. The Central Bank of Cyprus has safeguarded the banking sector against bad loans by granting it the ability of dynamic restructuring through both the decrease of installments and interest rates and the extension of the repayment period. In October 2014, out of the 28.2 billion-euro non-performing loans (49% of total loans), 11% was restructured. The restructuring percentage is expected to go up due to the insolvency law voted in January 2015.

3.2. Structural reforms

Cyprus, as with the majority of Southern European countries, has been accused of creating a cumbersome public sector due to the clientelism created between one-party governments and citizens. Regarding this aspect, the Cypriot government used the financial crisis and Troika as a scapegoat so as to justify significant and essential reforms. Specifically, from 2009-2014 the public sector shrunk by 4300 jobs while there were major reductions in the salary of employees on all income scales.

3.3. Privatizations

The bankruptcy of Cyprus Airways (9th January 2014) proved that the state can be not just a failed employer but a bad investor as well. The national air-carrier had been receiving distorting subsidies of 130 million since 2007. The subsidies contributed to the distortion of the competition in the air transport sector, leading the EU to the conviction of the Republic of Cyprus which eventually led the state-run company to bankruptcy.

At present, it is impossible for the state to sustain public and semi-public organizations without resorting to foreign lending or increasing the government deficit and by extension, the public debt. Under the circumstances and after significant pressure from Troika, the state is forced to proceed with large-scale privatizations. The main form privatization can take is through the sale of shares to institutional and strategic investors. In order to ensure the smooth operation and the social role of the organization, as well as to protect national interests, the state can retain a minority shareholding in these organization that will allow it to impose regulations and restrictions regarding their operation.

3.4.Discounting from the hydrocarbon reserves exploitation income

Preliminary research by the American energy giant Noble Energy firm has unveiled significant natural gas reserves in Cyprus’ Exclusive Economic Zone (EEZ) on the southern coast, reserves that could reach up to 6 trillion cubic meters. These preliminary studies can in no way determine the exact amount of the gas reserves, which is why it is impossible to draw conclusions as to the future production levels and future incomes. It is precisely for this reason that any conversation regarding the presale of a particular amount of reserves in order to alleviate the negative consequences from the current economic crisis is futile. Preoccupied with the Cypriot banking crisis, the markets do not seem to have positively discounted the possible impact on the state revenue from the sale of natural gas.

The extraction of hydrocarbons has, however, taken on a severe political dimension both on a regional and European level. The need to exploit these reserves has led Cyprus to the delimitation of its sea borders with Egypt (2003), Lebanon (2007), and Israel (2010). These agreements have drawn a strong reaction from Turkey, which threatens to obstruct any extraction attempts. Regardless of the way things will unfold, Cyprus, Egypt, and Israel have laid the foundations for a close commercial and energy cooperation that will play a determining role in their foreign policy.

3.5.Tourism

The exceptionally good weather conditions, excellent infrastructure, hospitable culture, and rich historical heritage have all made Cyprus one of the top tourist destinations of the Mediterranean and of Europe in general.

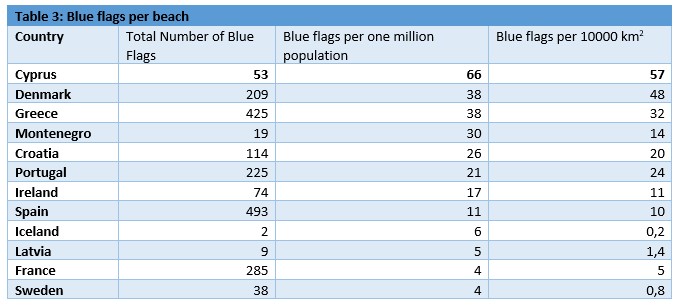

As can be seen in Table 3, based on the population and area size, Cypriot beaches have the greatest number of blue flags out of all the European countries.

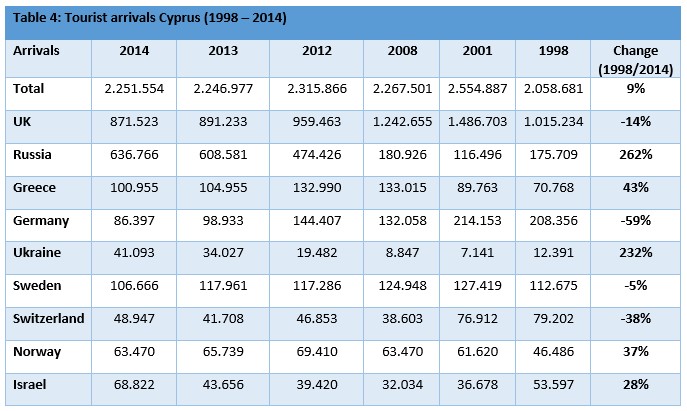

Table 4 shows tourist arrivals in Cyprus from the nine biggest markets for selected years between 1998 and 2014.

As can be seen, Cyprus was visited by 2.25 million tourists in 2014, approximately the same as in 2013. This number is lower by 12% compared to the record arrival year of 2001.

The biggest market in Cyprus is still the UK with 880 thousand tourists. This number is down by 30% compared to 2008, a milestone year for the UK economy since that was when the Lehman Brothers collapsed and offset the global economic crisis. After the strengthening of the sterling pound against the euro and with improved economic indicators in the country, British tourists are expected to return to Cyprus and based on predictions from the Cyprus Tourism Organization (CTO), they are expected to surpass 1 million by 2017.

The interest of local hotel and shop owners is nevertheless turned towards tourist influx from the second-largest market, Russia. Russian tourists that did not exceed 120 thousand in 2001 reached 630 thousand in 2014. Taking advantage of the presence of a large Russian community in Cyprus (40,000 permanent residents), the Cypriot market has created effective infrastructure and mechanisms to attract and serve Russian customers. The crisis in Ukraine and the consequent collapse of the rouble exchange rate has endangered the increasing trajectory of tourist movement from Russia. The latest indications nonetheless show that the decrease in tourism from Russia will be limited and will be limited to under 10%.

4.The factors undermining the stabilization efforts of the Cyprus economy

4.1.Political unrest in Greece

Due to their strong cultural and historical ties, Greece and Cyprus have developed equally powerful economic ties during the political changeover period. Their levels of cooperation are the following:

- Economic, commercial and banking relations

- Big tourist movement in both directions

- Common defense expenses due to a common defense doctrine

- Cultural ties

- Cooperation on an educational and university level

- A large number of immigrants from one country to the other

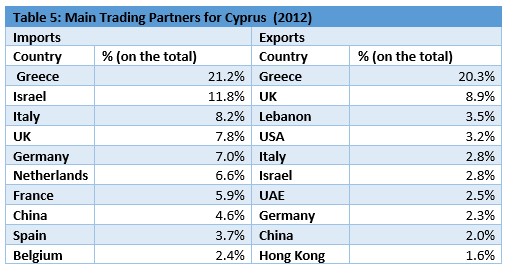

As can be seen in Table 5, Greece is the main trading partner for Cyprus both on an import and export level.

4.2.Non-performing loans

Bad loans of Cypriot banks have increased from 21 billion in June 2013 to 28.2 billion in October 2014, an amount equivalent to 48.95% of all loans. As has been previously mentioned, these loans are gradually going through a restructuring phase, but a dangerously large number of them has to be considered non-recoverable. Bad loans could create liquidity problems in the future and lead to a new recapitalization of Cypriot banks.

4.3.Lifting of the restrictive measures in the banking system

In December 2014, the Ministry of Finance announced the mitigation of three restrictions concerning the export of money abroad.

- For bank transfers abroad without a specification of purpose, the monthly amount has increased from €5,000 to €10,000.

- The number of banknotes being transferred abroad per journey has increased from €3,000 to €6,000.

- The payment or transfer amount abroad related to the usual business activities of the depositor has increased from €1,000,000 to €2,000,000.

The crisis in Greece and the pressure on its banking system could quickly spread to the banking system of the rest of the southern European countries, including Cyprus. These measures could come back, shattering the depositors’ trust once again.

4.4. Divestiture Bill

Under pressure from Troika, the borrowers’ inability to meet their financial obligations forced the Cyprus Parliament to vote for the divestiture bill that grants banks the power to confiscate and auction off the property. The bill opens up the way for mass confiscations and sales of property at particularly low prices. This procedure resembles that followed in the USA after the subprime mortgage loan crisis.

The promotion and sale negotiation for each property in consignments will not only be damaging for the owners but it will also be particularly time-consuming. Furthermore, an immediate sale to the public will bring substantial pressure to property prices, thus contributing to the worsening of the construction sector’s state.

In order to successfully execute divestitures, they need to be executed based on these two pillars:

- Categorization and insertion of properties into diversified investment packages that will include properties with different qualitative features. For example, agricultural land parcels with a limited sale probability can be sold as part of packages including attractive luxurious apartments in tourist zones. This way, the property of low quality that would otherwise remain as stagnant bank assets can be sold immediately.

- These packages must consequently be securitized and distributed for sale to selected strategic investors abroad. This way guarantees demand from institutional investors abroad, leaving property prices within the country unchanged.

The USA experience, as well as that from the rest of the Southern European countries (e.g. Spain), shows that the divestiture process will be particularly difficult and will not be immediately materialized due to the massive political cost it will have.

4.5. Upgrade of the pseudo-state and empowering of Turkey

Geopolitical balance in Eastern Europe and the Middle East is particularly fragile, but everything seems to help ensure the creation of an almighty Turkish economy and its political establishment as a key player in the global political chessboard. The political unrest caused by the elections of June 2015 with the weakening of the governing party is more of an indication of political purging rather than a destabilizing factor. From an economic perspective, the country’s GDP is rising at a rate higher than any other country in the EU because of its industrial development and the strengthening of its commercial relations with neighboring states.

The destabilization caused in the Islamic and Arab world from the appearance and expansion of the Islamic State (ISIS) seems to only be able to be halted by Turkey, Iran, and Saudi Arabia. The western countries coalition against ISIS led by the USA knows that and is therefore willing to make concessions on all levels to win favor and support from Ankara.

The empowerment of Turkey in the past decade has led to the indirect political and financial upgrade of the pseudo-state. The events that testify to the de facto strengthening of the pseudo-state in the last decade are:

- The opening of borders in April 2003

- The affirmative response to the ANNAN plan and the victimization of the Turkish Cypriots in the eyes of the global community

- The demand for the joint pooling of hydrocarbons with Turkish Cypriots, which gained a foothold in international diplomatic circles in 2014

- The significant increase of tourist traffic towards the occupied areas, both by Cypriots and foreigners

- The increase of construction activity and sale of holiday homes to foreigners

- The election of Mustafa Akinci, who is favorably inclined towards a solution, in April 2015

Conclusion

The stabilization of the banking system and the smooth carrying out of divestitures are the main mechanisms that can push the Cyprus economy towards growth rates in the coming 5 years, given the government’s attempt to promote the necessary reforms to control public debt and make the public sector healthier.

Indices

Index I: The financial crisis in Cyprus

The 2008 global financial crisis affected the Cyprus economy perhaps more than any other country in the world.

The causes that led to the collapse of the Cypriot economy are complicated and multifaceted. Due to filibustering from the prosecution authorities when it comes to examining the legal aspect connected to the crisis, the contribution of each institution and factor in the disaster has become impossible to currently identify.

At present, what can be done is a simple juxtaposition of these causes in chronological order, hoping that the result of the prosecutor’s investigation combined with the sincere event narration from the protagonists will allow us to classify the factors that led to the creation and deterioration of the crisis.

The operative event for the economic disaster in Cyprus was the cumulative global financial crisis that was offset with the collapse of the property market in the USA and led to the bankruptcy of Lehman Brothers on 15th September 2008. One of the first countries affected was the United Kingdom, which saw its GDP decreasing by more than 2.2% in 2009. The drop in British people’s purchasing power affected the Cypriot economy in two ways. The first was the freezing of purchasing interest for property in Cyprus, which contributed to the decrease of the general property index by 5% in 2009. The second way was through the mass booking cancellations from UK tourist agencies that caused a significant profit reduction in the tourist industry.

However, the biggest cause that contributed to the crisis was the irresponsible and dangerous bank investment policy.

After Cyprus joined the Eurozone on 1st January 2008, it became a particularly attractive destination for deposits for locals as well as European and third countries nationals. Initially, the incomparably high deposit interest rates that reached up to 6% led many Cypriots to lean towards the security of bank depositions. To be more specific, as can be seen in Table 2, between 2007 and 2010 Cypriots’ deposits in Cypriot banks increased by 40%. Secondly, the political unrest in Greece and the scenarios about a possible exit of Greece from the Eurozone (Grexit) led many Greeks to transfer their money to Cyprus. As the same table shows, the deposits of EU countries’ residents (which with an overwhelming majority belonged to Greeks) increased by 390% from 2007 to 2011. The most significant deposit flow nonetheless came from third-country citizens, and particularly from Russia. As a tax haven, Cyprus was the ideal destination both for Russian businesses and Russian capital. Solely during 2010, deposits of third-country nationals increased by 4.67 billion euro (+29.4%). In a country whose GDP was 19.5 billion euro in 2012, there were deposits of 70.1 billion.

Instead of using the massive deposit inflow as a tool for diversified investments on secure and promising industries around the world, banks preferred to “gamble” hoping to get “high yield” or distribute it to the masses in the form of housing and consumer loans.

Cypriot commercial banks, having gathered pools of money in their coffers and guided strictly by their instinct for financial gain, decided to take on the role of investment banks. The structure of a commercial bank, however, has massive differences compared to that of an investment bank. The most important of those is that the money under management for the former is comprised of deposits, while for the latter it is comprised of investments. Another significant difference is that the latter has both a wealth management fund as well as a risk management fund that allows it to select consistent and sensible investment strategies that will not expose the investors’ financial instruments or the own bank’s existence to any danger.

The first mistake was however accompanied by a greater one, which happened when they placed the largest share of those deposits in “toxic bonds” in Greece. It is doubtful whether any Criminal Court can effectively evaluate if that investment act constitutes a mistake and not a “litigious financial crime”.

The epilogue for the catastrophe began with the inevitable reduction (haircut) of the Greek bonds’ nominative value by 50% in 2011, leading the Cypriot banks to insurmountable liquidity issues. With the consent of the Central Bank of Cyprus, the banks resorted to lending from ELA (Emergency Liquidity Assistance). As was proven later, this was a wrong move to make since the banking system (especially the Popular Bank) was already under a state of bankruptcy and ELA’s contribution only served to further increase public debt.

Added to this series of devastating events was the destruction of Cyprus’ largest power station after the catastrophic explosion on the Evangelos Florakis Naval Base in Zygi in July 2011. The subsequent large-scale economic disaster led all international rating agencies to downgrade the Cyprus Republic’s creditworthiness and consequently increase its loan interest rates.

All of the aforementioned led to events that were brought into the global spotlight, like the ‘deposit haircut’ and the bankruptcy of the Popular Bank. Since then, Cyprus has been trying to get back on its feet.

Index II: The Divestiture Bill

The divestiture procedure for a property based on the bill that was passed by the Cyprus Parliament consists of the following stages:

- Independent assessment by a valuator assigned by the bank to which the property is mortgaged and one assigned by the owner.

- If the two estimates significantly diverge, a third independent evaluator will be called upon to assess the property. After the third estimate, there will be an agreement as to the final “fair” sale price of the property that will reflect the general conditions in the property market.

- On the first stage, there will be an attempt to estimate the property at a price of no less than 80% of its final estimated value. The 80% limit will stand for a period of three months.

- On a second stage and in case the property is not divested on the first attempt, the new sale limit will be set at 50% of the property’s final estimated price. The 50% limit will last for a period of nine additional months.

- After the two stages, there will be a new valuation process of the property in order to set a new fair final price. In this case, the property can be sold for up to 50% of that estimated value.