1. Introduction:

Investment funds or mutual funds industry is one of the most growing in the global financial system. There are more than 78000 registered funds in the financial market. From July to December of 2014 it is estimated that their worldwide value is $32 billion, which is 35% more than that in 2011.

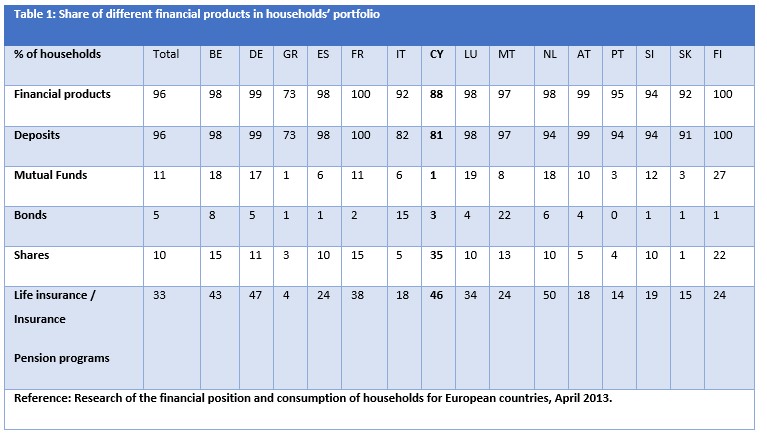

Mutual funds play a crucial role in family budgets as well. The contribution of mutual funds in the average household portfolio of the US is four times bigger today in 2013. Table 1 shows that 11% of the households in Europe maintain mutual funds in their portfolio and in some cases such as Finland the percentage can go up to 27%.

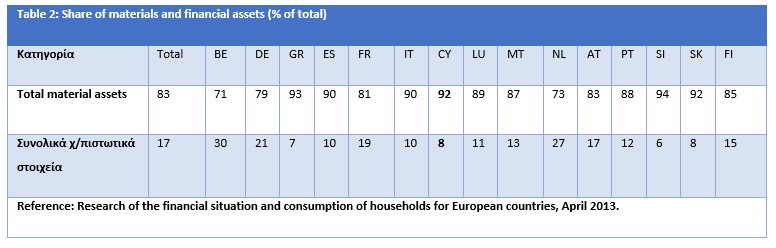

However, in the case of Greece and Cyprus mutual funds do not seem to be a popular choice. As it is shown in Table 1, the share of mutual funds in Greek and Cypriot households reaches 1%, which is the lowest percentage in the Eurozone. This percentage, in reality, reflects a much smaller percentage if we consider that from the aggregate assets only the 7% - 8% is invested in financial products (Table 2)

Table 1 shows that Cypriots hold a significant number of stocks in their portfolio, i.e. financial products of high risk and volatility, making this percentage as the highest in the Eurozone.

This is contrary to the assumption that low-risk financial products are more common in Cyprus; such as private pension programs and life insurance. The percentage of Eurozone is 45, 7%.

This paper involves a presentation of the characteristics and the role of investment funds. Moreover, it examines the reasons behind the slow development of mutual funds in Cyprus, and finally, it refers to how mutual funds can help investors reach their investment targets.

2.Definition and characteristics of investment funds:

Investment funds consist of mechanisms that concentrate monetary funds from a huge number of investors to a mutual pool, which is then invested in different financial assets classes such as bonds, shares or properties. This pool can be an independent legal entity or a simple investment bank. The fund manager with his/her investment team is responsible for the allocation of monetary funds into the different asset classes.

Investment funds can be classified by their:

A.Structure:

- Closed-ended funds: It is an investment vehicle that buys stocks in the market. Shares of the close-end fund are traded in the stock market at a price determined by supply and demand for that fund. The fund’s market price can differ from the value of the assets held in its portfolio, which is the NAV. The number of shares usually remains fixed and shares cannot be redeemed but are only traded in the stock market.

- Open-ended funds or mutual funds: Publicly offered and its shares can be purchased and redeemed at the Net Asset Value (NAV) of the assets owned by the fund.

Mutual funds are the most common funds from the two types. The closed-ended fund manager concentrated investors’ money in a mutual pool and then buys financial products. The share value is equal to:

Share value = NAV/ Number of shares = NAV – obligations/ Number of shares

B. Riskiness:

- Low risk: Those funds are invested in deposits, money funds and government bonds of developed countries.

- Medium risk: Investments in corporate bonds of multinational companies and government bonds of developed countries.

- High risk: Investments in shares, government bonds with low creditworthiness, corporate bonds of small corporations and financial instruments, (options, futures, CDF).

C. Investment product:

- Money market funds

- Bond funds

- Fixed income funds

- Stock or equity funds

- Hybrid funds

D. Active management degree:

- Active management funds: Fund managers and their investment teams try to select financial products of preferred risk-return characteristics based on technical and fundamental analysis.

- Passive management funds or index funds: Funds that follow the investment strategies of indexes such as the FTSE or Dow Jones. According to Warren Buffer (probably the best investor of the 21st century), passive management funds are ideal for the average investor. In the US, between 2002-2012, 40% of mutual funds failed to reach the average index despite their complex financial analyses.

E. Sector: For example, there are investment funds that invest only in the automotive industry, manufacturing industry, gold, renewable, etc.

F. Geographic region: Investors can experience funds invested only in countries of the Eurozone, USA, Southeast Asia, Central Africa, etc.

3. Providers of investment funds in Cyprus and the role of the insurance industry:

In Cyprus, the main providers of mutual funds are insurance companies, banks, and a small number of investment corporations.

The role of the banking system:

In industrially developed counties where the regulatory framework of financial services is very strict, the banking system is divided into commercial and investment banks and differentiates their tasks. Investment products such as investment funds are offered to the general public by investment banks. In Cyprus, banks, because of overriding their monopoly position in the financial system and their close relationship with the government, they managed to prevent this distinction. As a result, commercial banks created high-risk investment funds, which they were presented to the general public as safe and high return investments. Therefore, these funds became attractive to Cypriot people who converted their deposits into investment funds with high risk, (debentures). Debentures’ money mostly invested in Greek public and private bonds which initially offered huge profits because of the expanded spreads.

However, banking institutions did not limit their exposure only to debentures. Greek junk bonds attracted Cypriot bankers due to their high level of returns; they used their deposited money to buy more and more. This kind of transaction was not illegal since every bank can maintain its investment strategies in accordance with the national central bank’s guidelines. However, the previous situation could be characterized as a financial crime, and led to the well-known “haircut” since all “eggs went into the same basket”.

The banking crisis in combination with the long-term mismanagement of the banking funds led the government to a new and stricter way of promoting financial products from the banks. Today commercial banks are not allowed to offer investment products or investment funds.

The role of investment companies:

Investment companies operating in Cyprus have experienced a large decrease in the number of their customers; however, they still offer a wide range of financial products with regards to portfolio management. Furthermore, the last decade brought into the surface a large number of independent investment funds in the form of open-end and close end. Their basic disadvantages are that they charge high management fees, which in turn limit any advantages of high returns and differentiation. Also, trust issues became a problem since those companies are small in size with limited experience, while there is always the danger that some of them to be a form of a Ponzi scheme, which allocates to their old customer's money invested by new customers.

Beyond the domestic investment companies, the financial crisis in Cyprus created some space for the growth of international investment companies, which operate through telephone calls and look like an alternative solution for the Cypriot depositor. Trust issues and the fact that their yields are taxable outside the country are some of the dangers faced with this kind of company.

The role of insurance companies:

The main provider of investment funds in the Cypriot economy is insurance companies.

In contrast with the regulatory agencies of the financial system of other developed counties, the Securities Commission in Cyprus does not allow insurance companies to sell mutual funds as independent investment products, such as pension and student packages. However, it does allow the sale of different categories of investment funds connected with life insurance and medical care. Specifically, each licensed insurance company that sells life insurance is obligated to create investment funds with different levels of risks, in which it will invest its customers’ money. Pension schemes started becoming more popular in the last five years, which, however, are connected with life insurances. The latter fact can help explain the high percentage of Cypriots who have in their position pension insurance products.

Insurance companies publish the composition of their investment funds. Also, they are often obligated to make sure their customers are up to date with any changes and the reasons for those changes in their investment strategies. The financial crisis affected significantly the investment policy of insurance companies in Cyprus. The funds invested were removed from Cyprus and Greece to less risky investments in West Europe. The exposure of Cyprus to Cypriot banks cannot be nullified because of the close relationships and interdependence between the banking and insurance systems. Moreover, financial products of low risk such as government and corporate bonds were now preferred for portfolios (instead of shares).

4. Pros and Cons of mutual funds:

4.1 Pros of mutual funds:

Differentiation and reduction of investment risk:

Mutual funds diversify investment funds being managed into different countries, industries, and classes of products, thereby reducing systematic risk.

The financial theory assumes that in a portfolio of 30 shares could offer differentiation and significant reduction of risks. However, new financial theories show that in a globalized economy, even a portfolio of 1000 shares cannot reduce significantly systematic and unsystematic risks. For a portfolio to reduce those risks, it should be differentiated and invested in different sectors of the economy of different countries and different financial products.

High liquidation investment:

The majority of mutual funds (open-end funds) can be easily liquidated just like shares do. Insurance companies in Cyprus

The accessible minimum amount of investment:

Only wealthy investors could participate in mutual funds in the past. However, every investor, irrespective of his/her economic situation, can invest in mutual funds in a variety of ways and with small amounts of money.

Wide range of choices:

Every investor can invest in the investment fund of his/her choice depending on his/her preferences and beliefs. For example, an individual who believes that the Chinese automotive industry will rapidly grow in the future could invest in a particular mutual fund.

The rapid growth of savings principle:

Mutual funds that offer the opportunity of monthly subscription encourage the principle of savings. Investors who are aware and are willing to save money for the future are highly motivated to participate and reach their targets.

The vast majority of investors do this through investment funds for pension, children studies, future self-employed opportunities or the purchase of a house, etc.

Tax-free:

With regards to insurance companies both the insured amount and the value of the purchase are tax-free if they are legally reported.

Professional management:

Nowadays, the global economy can be characterized as very complex since thousands of variables are anarchically involved in the market. It is impossible for an individual investor to be up to date with the economic and political news on a 24-hour basis. Therefore, technical and fundamental analysis concerning changes in the prices of assets, bonds, macroeconomic variables, commodities, etc cannot be done by an individual investor all the time. Huge investment funds have experienced analyst teams from different scientific fields, who can use sophisticated statistical packages and perform rapid risk and cost assessments. Moreover, bigger funds have political consultants and people coming from big multinational companies and who can access information not readily available to the general public.

Concentrated investment power and access to investments that are only available to large institutional investors:

Let us consider an example to make this advantage clear to everyone. At the beginning of the 21st century, it was already clear that the Chinese economy, based on the GDP growth figures, was becoming stronger again. Investors were also aware of the growth prospects of the property market. Ongoing analyses and publications in the international financial press commended the work of the Chinese government concerning the liberalization of the market while emphasizing the huge capital flows that contributed to the creation of a dynamic, in terms of demand for commercial and residential real estate, in major states of the East Coast. However, how could a single international investor benefit from this? Big investment banks and companies such as JP Morgan and Blackrock were making massive investments (billions of money) on properties. They were given the permission of the Chinese government, while, at the same time, they were creating investment packages that institutional investors had access to, (minimum investment millions of money).

Surface:

The operation of mutual funds is fully transparent. Mutual funds are obligated to show in their annual reports their investment targets as well as the percentages that are allocated to the different product classes. Also, they are obligated to publish reports and financial statements on a three month and six-month basis.

Change of investment fund (insurance companies):

Insurance companies in Cyprus offer the possibility to investors to move their funds between the investment funds depending on their preferences and without any additional costs.

4.2 Cons of mutual funds:

Restrictions regarding investment destinations:

The Cyprus Securities and Exchange Commission raises significant restrictions on the investment choices of insurance companies’ investment funds that lead away from investments other than perfect investments, thereby reducing their expected average odds. Firstly, investment funds that are insured are obligated to maintain a huge percentage of their funds in the form of deposits in Cypriot banks. Secondly, investments in hedging products are not allowed (e.g. futures, options, etc), which contribute significantly to the profitability of an investment portfolio.

Restrictions regarding odds:

Investment funds do not respond to risk lovers since their primary target is the reduction of risk and not high yields.

Risks are never nullified:

Despite the differentiation that exists in the mutual funds market, systematic risk will always exist. Systematic risk is the risk of a general global or national crisis. Practically, this means that for risk-averse investors, this alternative will never be attractive. Investors will always choose to invest their money in banks, gold, or government bonds that provide guaranteed returns.

The haircut of Cypriot deposits in March 2013 led to rumors regarding whether bank deposits are guaranteed. Professional managers of mutual funds state that a safer alternative for investors’ money is to invest them in mutual funds of an international range which have high creditworthiness, instead of investing them in banks with risky assets.

Low season:

Mutual funds have the possibility of instant liquidation. However, this is not the case with mutual funds that are connected with insurance or pension packages. In the case of insurance contracts, there is an initial period of one or two years that the cash value is not paid to cover the cost of the insurance. A pension program usually offers restricted withdrawals in the first five years or they do not allow high yields.

High management costs:

Management costs of mutual funds are differentiated depending on their active management degree. The basic form of charge that the investor pays in a fund is the management fee that is related to the financial product selection progress. Customers that want to avoid high management fees can go with passive management funds.

Lack of effective differentiation:

Managers of mutual funds, sometimes, ignore the theory of differentiation due to the high odds and thus creating portfolios that involve products with identical economic characteristics and with the identical degree of sensitivity to the different macroeconomic variables.

The regulatory framework of the banking system:

In the US, the central regulatory authority is the Federal Reserve, whose primary aim is to maintain inflation at low levels and the reduction of unemployment. Bank deposits are guaranteed through an organization called FDIC (Federal Deposit Insurance Corporation), and which guarantees deposits up to $250000. This is the highest guaranteed amount of money than any other organization globally. However, what if all FDIC depositors wanted their money today? How could FDIC be able to deal with such a scenario? Based on the latest statistics, bank deposits in December 2014 in the US were more than $11,7 trillion, whereas FDIC had in its position cash and assets valued at approximately $50 billion, and with the possibility of borrowing another $50 billion from the Ministry of Finance. Practically, this means that in case of a banking bankruptcy 96% of bank deposits will fail. This scenario has been confirmed during the great crisis in 1930 when 4000 US banks went into bankruptcy in 1933 and 9000 in total during the 1930 decade. During the 1930 decade, deposits of $140 billion have been disappeared. The supreme mortgage crisis in 2007 drove 65 banks into bankruptcy with total deposits of $55 billion.

The European banking system is in even a worse situation. Based on the revised instructions of the European Parliament, in European countries, the first 50000 euro of each depositor is guaranteed. The majority of European governments guarantee the first 100000 euro from all deposits, but without analyzing how they will react in case of a banking crisis. Moreover, the European Central Bank (ECB), which is the regulator of the European system, does not mention in its statute that it has an obligation to intervene and rescue any European country’s banking system in case of default. For example, the ECB showed no intention to rescue the Cypriot banks in 2013. The debt crisis of Southern Europe forced the leader of the European Union to the creation of the European Stability Mechanism in September 2012, with the primary aim to rescue the banking system. European Stability Mechanism has the power to lend up to 500 billion euros. However, this number is inadequate if we assume that the total number of deposits in the Eurozone stands at 20 trillion euros. Unsurprisingly, only in Greece, the amount of banking deposits is approximately 145 billion euro.

The framework that central banks follow to regulate the banking system is based on Basel Accord ll. This is divided into three pillars. The first pillar sets the limits of the minimum capital requirements that have to be maintained by the banks to be healthy. The second pillar determines the regulatory framework and the third pillar sets the transparency framework. In the European Union, the Basel’s regulations are implemented based on the Capital Requirement Directive. The latter forces banks to maintain in cash (or easily liquidated assets) the 15% of total loans that have been lent outside. Assuming that banks lend more money than the money coming in the banks in the form of deposits, is it pretty clear that they cannot respond to a massive request of at least 15% of their customers’ deposits.

The size of the insurance industry:

Based on the latest statistical data of the European Insurance Federation, the insurance industry in 2012 consisted of 5300 insurance companies with total management funds of 8, 4 trillion euros. French insurance companies have the largest funds in Eurozone that stand up to 1, 65 trillion.

In Cyprus, the industry consists of 34 insurance companies which in total have assets valued at 1, 8 billion euro, and with the investment funds of life contracts to have a total value of 1, 6 billion euro.

Based on the same research, the total compensations that have been paid in 2012 by the insurance industry of Europe were 948 billion euros. More than 68% of this number was given for the benefits of contracts in life insurances.

The investment policy of insurance companies, after the financial crisis, became particularly conservative. Investments in shares are avoided, 50% of funds are lent out as loans to small or medium enterprises, while a big amount is invested in fixed-income assets such as bonds and deposits.

The regulatory framework of the insurance industry:

In contrast to banks, there is no single body that regulates insurance companies. What exists is an extensive mutual system. National and local insurance companies are also insured by other multinational insurance companies called reinsured, and which are insured between them. This system ensures the adequate spread of risk since if a single insurance company faces problems in responding to its obligations, its reinsurance company takes over the responsibility and pays the customer. In this way, even in cases of natural disasters, national insurance companies have the ability to pay out huge amounts of money from their reinsurance companies, without exposing themselves.

Despite the absence of a mutual regulatory framework, the European insurance companies follow a mutual regulatory framework of three pillars, called Solvency ll Directive, and which will officially be implemented from the 1st of January 2016. The way that Minimum Capital Requirements and Solvency Capital Requirements of insurance companies are set, is way more complicated than banks’ requirements.

In practice:

The profitability of insurance companies is not based on lending (like banks. Insurance companies are obligated to have in their funds at least the amount of funds that cover the probability of a massive claim of their active life insurance contracts from their customers in their portfolios. Once again, the big recession in the US became the ultimate test with the majority of insurance companies to be in the position of immediate payment of all of their active contracts of their clients. Despite the banking crisis in Cyprus and the haircut of deposits, insurance companies were able to pay their customers’ claims and avoid being bankrupt.