WHAT IS IP BOX REGIME?

The IP Box regime is a company tax regime used by some countries to stimulate research and development activities.

In Cyprus, this regime is mainly used by companies producing computer programs. Thanks to the benefits provided by it, one of the largest game development companies, Wargaming, has relocated to Cyprus.

The IP Box regime provides companies with tax incentives for the income derived from qualified intellectual property (licenses, sub-licenses, sale and/or transfer of intellectual property assets). Intellectual property (hereinafter - IP) is the result of any intellectual activity, like computer programs, mobile applications and video games, innovative algorithms and formulas, inventions, trade secrets and know-how, industrial practices, marketing concepts, works of art, designs, images, names and inventions used in trade.

Intellectual property is one of the most valuable assets of a company. One of the advantages of most IP assets is the lack of a fixed geographic reference. Because of its non-physical nature, intellectual property is also convenient to work with.

An IP object can easily be relocated between different jurisdictions at no significant cost, depending on the circumstances and the tax systems. 85% of multinational companies use this advantage to reduce the overall tax burden by allocating valuable intellectual property to those companies of the group that are registered and operate in the countries with the most tax-friendly IP Box regime. Today more than 2,000 IT companies use Cyprus as their tax base, while the bulk of their operations are carried out abroad.

KEY FEATURES OF THE IP BOX REGIME IN CYPRUS

Before moving on to the peculiarities of Cyprus's regime of taxation of intellectual property, it is necessary to determine which IP objects are classified by the legislation of Cyprus as qualified IP objects (assets) used in the taxation under the IP Box scheme. Qualified IP objects in Cyprus include:

- Patents (as defined in the Patent Law).

- Copyright-protected computer programs (including mobile applications and video games).

- Other intangible assets classified according to the principle of usefulness and novelty.

Qualifying IP objects do not include names, brands, trademarks, copyrights, images, and other marketing rights.

In accordance with the Cyprus IP Box regime, the following are exempt from corporate tax:

1) 80% of the profit from the sale of intellectual property right.

80% of the profit from the sale of the related intangible assets is not recognized for tax purposes. This is a significant exception compared to other regimes (see the table below).

2) 80% of the income from the use of intellectual property rights.

Four-fifths (80%) of the income generated from the use of intangible assets are deductible for tax purposes. Thus, only 20% of IP revenue after deducting the revenue generation costs is taken into account. Thus, Cyprus' corporate tax rate of 12.5%, which is one of the lowest in the EU, provides an effective tax rate of 2.5%.

Apart from that, the Cyprus IP Box regime offers the companies a 5-year amortization period for IP capital expenditures.

Capital expenditures related to the acquisition or development of intellectual property can be deducted in the first tax year in which these expenditures were incurred, as well as in the next 4 years. In practice, this can bring the effective tax rate down to less than 2%.

KEY DIFFERENCES BETWEEN COUNTRIES USING THE IP BOX REGIME

Countries are striving to attract innovative businesses by providing reduced tax rates for companies that have established proper accounting for intellectual property rights and related cross-border transactions.

One jurisdiction may be better than others in some aspects, while another may offer different benefits. The similarities and differences, advantages, and disadvantages of jurisdictions need to be evaluated and compared with each other based on the particularity of a specific company and the main characteristics of a potential jurisdiction in order to make the best business decision.

Below we have provided a table that shows the main characteristics of IP Box regimes operating in different European countries.

| Country | Cyprus | Belgium | Hungary | Luxemburg | Netherlands | France | United Kingdom |

| Effective Tax Rate, % | 2.5% | 4.44% | 4.5% | 5.2% | 7.0% | 10.0% | 10.0% |

| Qualifying IP objects | Patents, computer software, utility models, other IP rights assets like non-obviousness, usefulness and originality (novelty) | Patents and additional patent certificates, copyrighted software |

Patents,

utility models,

|

Patents, trademarks, designs, domain names, models and software copyrights, brands for services for goods, like manufacturing and marketing know-how | Proprietary intellectual property related to patents, copyrighted software, or approved research and development |

Patents, service certificates, copyrighted software

|

Patents and similar rights |

| Invalid objects of intellectual property | Company names, trademarks, image rights, marketing activities | Know-how, trademarks, designs, models, formulas and processes | Design | Formulas, copyrights (excluding software) | Trademarks, brands and acquired intellectual property |

Non-patentable inventions, R&D |

Trademarks, copyright and design |

| Internal development or acquisition? | Proprietary IP, designed and acquired | IP rights developed independently or acquired or licensed from third parties | Proprietary IP, designed and acquired | IP developed and acquired internally, but not IP obtained form a related party | Only proprietary IP developments | Proprietary intellectual property, designed and acquired | Proprietary intellectual property, designed and acquired |

| R&D restrictions | Yes | Yes | No | No | Yes | No | No |

| Income subject to the regime |

Royalties, license fees, compensation income, trading profits from the sale of IP, capital gains from the sale that are not subject to any tax |

Patent income | Royalties | Royalties net of costs (depreciation, R&D costs, percent) | Net income from qualifying assets | Net profit from licensing, sublicensing or sale of certain IP rights | Net income from qualified IP |

| % reduction in tax rate | 80% | 85% | 50% | 80% | Irreducible tax rate | Irreducible tax rate | Irreducible tax rate |

| Is there a limit to the decline in profit? | No | 100% profit before tax | 50% profit before tax | No | No | No | No |

| Sales profit included? | Yes | No | Yes | Yes | Yes | Yes | Yes |

SUMMARY OF THE COMPARISON OF IP BOX REGIMES IN EUROPEAN COUNTRIES

Based on the data in the comparison table it can be concluded that the Cyprus IP taxation scheme is the most flexible and efficient one compared to the schemes offered by other European countries:

- The Cyprus IP Box regime provides for a maximum tax rate of 2.5% on the income derived from intellectual property assets. Its closest competitors with a comparable indicator are Belgium - 4.44%, Hungary - 4.5% and Luxembourg - 5.2%, with their tax rate being, however, almost twice as high. They are followed by the Netherlands with 7%, and France and Great Britain with a 10% lag falling slightly behind the Netherlands, but far behind Cyprus.

- The Cyprus IP Box regime applies to a wider range of income compared to other similar European schemes, most of which limit the benefits to the income from patents and additional patent certificates.

- While IP Box regime schemes in Belgium, Hungary, Luxembourg, the Netherlands, and the United Kingdom offer partial exemptions from sales profits, their benefits become less attractive to IP holders than those offered by the Cyprus scheme due to their restrictions on qualifying assets and a smaller rate cut.

CALCULATION OF THE CORPORATE TAX OF A CYPRUS COMPANY WHEN USING THE IP BOX REGIME

TABLE. EXAMPLES OF CALCULATION OF THE CORPORATE TAX WHEN USING THE IP BOX REGIME

| Variant 1 | Variant 2 | Variant 3 | Variant4 | |

|

"Qualifying Assets" are designed, created and then improved by the company itself. All R&D was carried out independently, nothing was outsourced. | "Qualifying Assets" - purchased by a Cypriot company ready-made. R&D was outsourced to an unrelated party for further improvement. | "Qualifying Assets" - acquired by a Cypriot company ready-made. R&D was outsourced to a related party for further improvement. | "Qualifying Assets" - acquired by a Cypriot company ready-made. R&D was outsourced to a related and unrelated party for further improvement. |

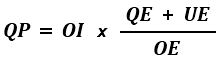

| Overall Income (OI) (Revenue-Direct Costs) |

1,000,000 Euro | 1,000,000 Euro | 1,000,000 Euro | 1,000,000 Euro |

| Overall Expenditure (OE) | 500,000 Euro | 500,000 Euro | 500,000 Euro | 500,000 Euro |

| The cost of acquiring qualifying assets | 0 Euro | 300,000 Euro | 300,000 Euro | 200,000 Euro |

| R&D Expenditure transferred to a related party | 0 Euro | 0 Euro | 200,000 Euro | 75,000 Euro |

| Qualifying Expenditure (QE) EXCLUDED: costs of acquiring qualifying assets and costs of R&D outsourced to a related party |

500,000 Euro | 200,000 Euro | 0 Euro | 225,000 Euro |

| R&D Expenditure carried out by the company itself | 500,000 Euro | 0 Euro | 0 Euro | 200,000 Euro |

| R&D Expenditure transferred to an unrelated party | 0 Euro | 200,000 Euro | 0 Euro | 25,000 Euro |

| Uplift Expenditure (UE) (the lower of the two values is used for the calculation) |

||||

| 30% of the total size of the Qualifying Expenditure (QE) | 150,000 Euro | 60,000 Euro | 0 Euro | 67,500 Euro |

| The costs of acquiring qualifying assets + RD costs transferred to a related party | 0 Euro | 300,000 Euro | 500,000 Euro | 275,000 Euro |

| Qualifying Profit (QP) | 1,000,000 Euro | 520,000 Euro | 0 Euro | 585,000 Euro |

| Tax incentive (80%) | 800,000 Euro | 416,000 Euro | 0 Euro | 468,000 Euro |

| Taxable income (Total income minus tax incentive) |

200,000 Euro | 584,000 Euro | 1,000,000 Euro | 532,000 Euro |

| Tax amount (at the rate of 12.5%) | 25,000 Euro | 73,000 Euro | 125,000 Euro | 66,500 Euro |

Thus, the greatest benefit in terms of taxation in Cyprus is received by the companies that create and improve intellectual property products independently.